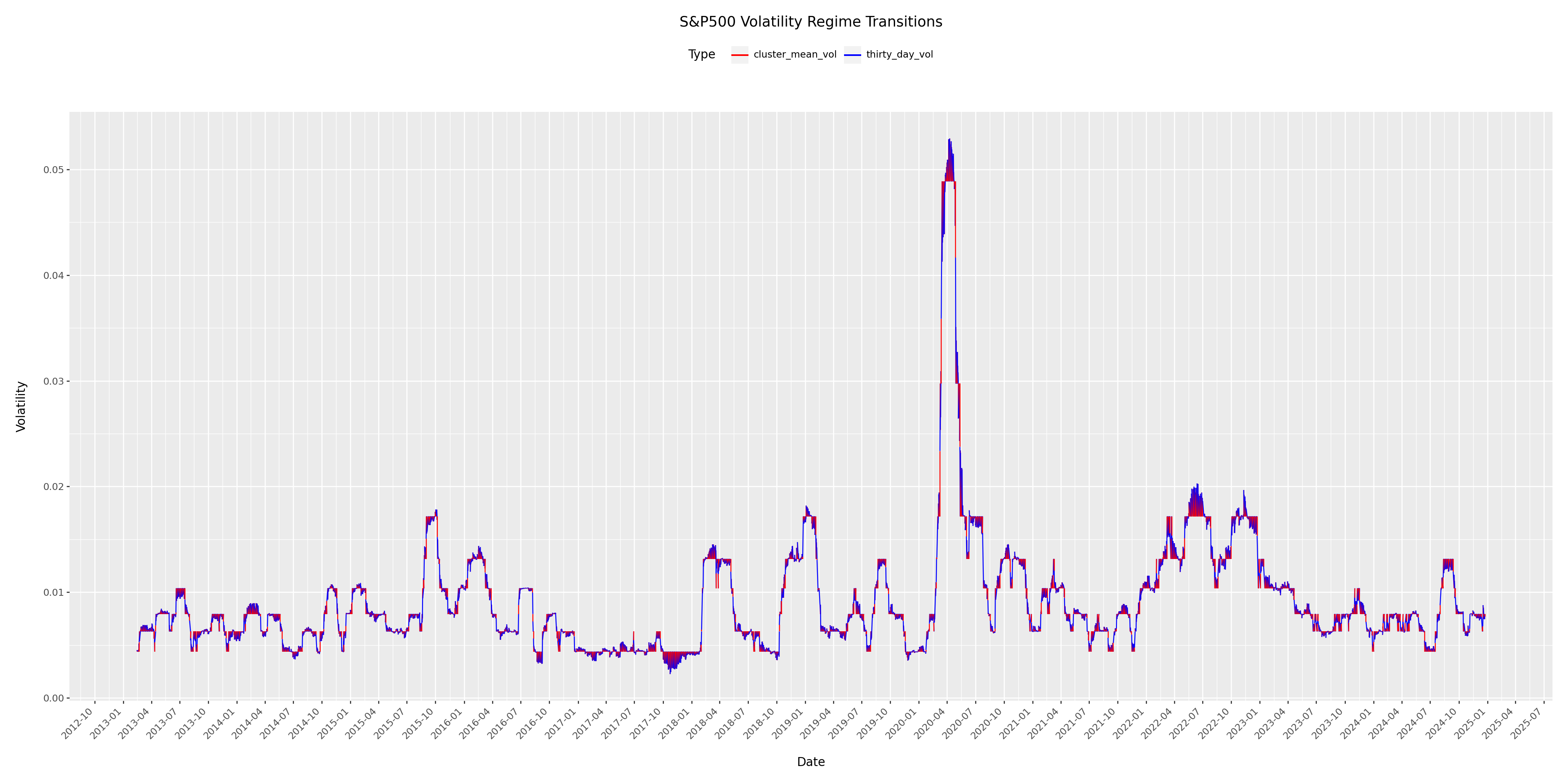

Goal: Use the broad stock index to model and understand the index volatility levels.

Key methodology: Use KMeans to build clustering model and then volatility regimes and then build transitional probability distribution among the regimes

Import Library

Code

import pyprojrootfrom pyprojroot.here import hereimport osimport yfinance as yfimport pandas as pdimport numpy as npimport ibisimport ibis.selectors as sfrom ibis import _ibis.options.interactive =Trueibis.options.repr.interactive.max_rows =20from plotnine import ggplot, geom_line, geom_path, aes, facet_wrap, labs, scale_x_continuous, theme, element_text, scale_y_continuous, scale_x_date, scale_color_manualimport matplotlib.pyplot as pltfrom sklearn.cluster import KMeansfrom sklearn.preprocessing import MinMaxScaler

# Define the ticker symbol for the S&P 500 indexticker ='^GSPC'# Define the start and end datesstart_date ='2013-01-01'end_date ='2024-12-26'# Fetch the historical datasp500_data = yf.download(ticker, start=start_date, end=end_date, multi_level_index=False).reset_index()# Display the datasp500_data.head(10)

Date

Close

High

Low

Open

Volume

0

2013-01-02

1462.420044

1462.430054

1426.189941

1426.189941

4202600000

1

2013-01-03

1459.369995

1465.469971

1455.530029

1462.420044

3829730000

2

2013-01-04

1466.469971

1467.939941

1458.989990

1459.369995

3424290000

3

2013-01-07

1461.890015

1466.469971

1456.619995

1466.469971

3304970000

4

2013-01-08

1457.150024

1461.890015

1451.640015

1461.890015

3601600000

5

2013-01-09

1461.020020

1464.729980

1457.150024

1457.150024

3674390000

6

2013-01-10

1472.119995

1472.300049

1461.020020

1461.020020

4081840000

7

2013-01-11

1472.050049

1472.750000

1467.579956

1472.119995

3340650000

8

2013-01-14

1470.680054

1472.050049

1465.689941

1472.050049

3003010000

9

2013-01-15

1472.339966

1473.310059

1463.760010

1470.670044

3135350000

Clean data with ibis framework. We only need to keep Date and Close columns. Since data is downloaded live, we also archive a copy of data.

It is totally okay to use Pandas to clean the data. It’s just a personal preference that I prefer the modernized and portable syntax of ibis framework.

Code

# import to duckdb backend of ibis frameworksp500_data_ibis = ibis.memtable(data=sp500_data)sp500_data_cleaned = ( sp500_data_ibis.select("Date", "Close") .mutate(Date = _.Date.date(), Close = _.Close.round(digits =2)))# export a csv copysp500_data_cleaned.to_csv(path = os.path.join(output_dir, "sp500_close.csv")) # preview of datasp500_data_cleaned

return_window = ibis.window(preceding=30, following=0, order_by="Date")sp500_data_transformed = (sp500_data_cleaned.mutate(Previous_Close = _.Close.lag()) .mutate(Daily_Return = ((_.Close - _.Previous_Close)/_.Previous_Close).round(digits =6)) .mutate(thirty_day_vol = ibis.ifelse( _.Daily_Return.count().over(return_window) >=30, _.Daily_Return.std().over(return_window).round(digits =6), None)))sp500_vol_no_null = sp500_data_transformed.filter(_.thirty_day_vol !=None)sp500_vol_dates = sp500_vol_no_null.select("Date").mutate(index = ibis.row_number())sp500_vol = sp500_vol_no_null.select("thirty_day_vol")# bring to pandas dataframes to be more compatible with sklearn APIssp500_vol_pd = sp500_vol.to_pandas()

Train KMeans Model

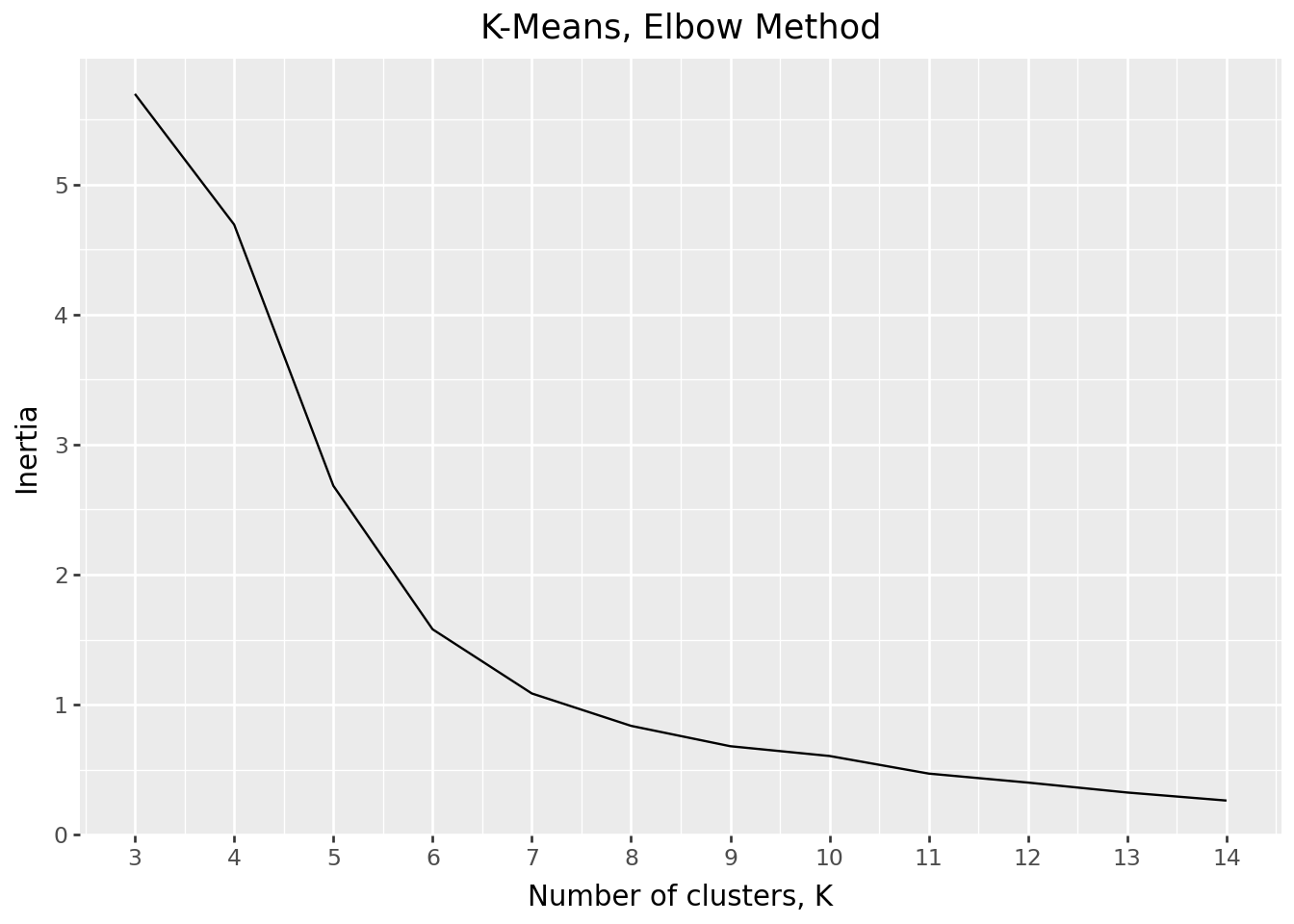

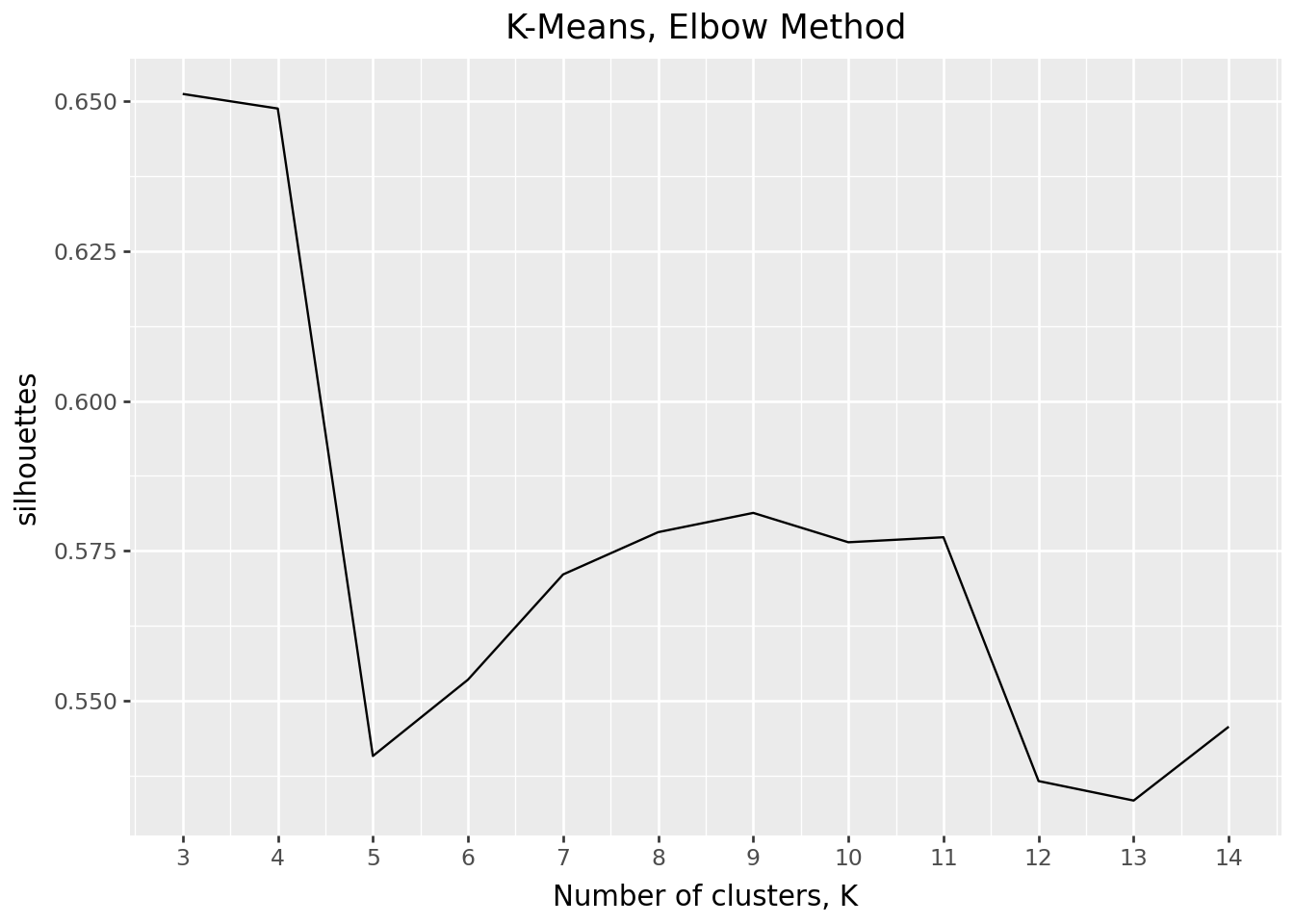

Find the Optimal K, using elbow method

In the following “elbow charts”, trade off between inertia and silhouette scores, we settle at 9 clusters, as it gives a relatively high silhouette scores whil keeping a relatively low inertia.

sp500_vol_pred = ( ibis.memtable(data=sp500_vol_pred)# adding the dates back to the volatility dataset .mutate(index = ibis.row_number()) .left_join(sp500_vol_dates, "index") .select(~s.startswith("index")))( sp500_vol_pred.aggregate( by ="cluster", count = _.thirty_day_vol.count(), mean = _.thirty_day_vol.mean(),max= _.thirty_day_vol.max(), median = _.thirty_day_vol.median(), min= _.thirty_day_vol.min()) .order_by(_.cluster))

# get a frequecy of each cluster to calculate relative frequency of each transition type, see belowsp500_cluster_vol_count = ( sp500_vol_pred.aggregate( by ="cluster", count = _.thirty_day_vol.count()) .mutate(cluster = _.cluster.cast("String")))vol_transition_table = (# perform crosstabbing between cluster_from and cluster_to to understand count of transitions sp500_vol_pred_shifted .mutate(counter =1) .pivot_wider(names_from ="cluster_to", values_from="counter", values_agg="sum", values_fill=0, names_sort=True)# add cluster frequency .left_join( right = sp500_cluster_vol_count, predicates= _.cluster_from == sp500_cluster_vol_count.cluster )# clean up data .drop(_.cluster_from) .order_by(_.cluster) .relocate(_.cluster, before="0"))vol_transition_table